What We're Reading #20

India's export credit scheme, the Sun Pharma-Organon deal, what a fruit says about China, and the contours of the rupee.

Hi folks, hope you’ve had a great week!

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’ve started “What We’re Reading”, where every weekend, our team outlines the interesting articles — even books — that put our brains in seventh gear (if that even exists).

We also host a book club every Saturday that we talk about at the end. If you’d like to read with us, please feel free to join!

We’d also love to know what has piqued your interest, too! Please feel free to let us know in the comments.

What Kashish is reading

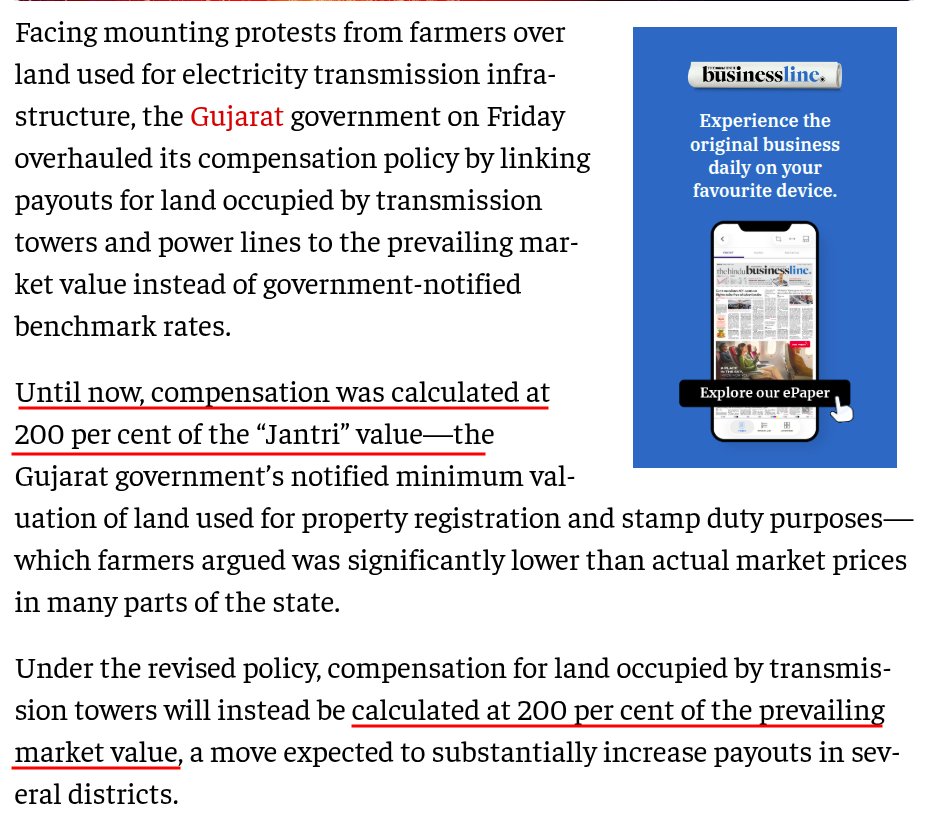

Gujarat’s new land acquisition policy for transmission lines (link)

According to Ember, India curtailed around 300 GWh of renewable energy in Q1 2026 because the grid simply couldn’t carry it. That’s nearly two-thirds of all renewable curtailment across the country.

The obvious solution is to build more transmission lines. But transmission is expensive, and after Gujarat’s recent policy changes (it produces and curtails the most solar), acquiring land for new lines could become even more costly.

So what if the answer isn’t just building more supply—more solar, more batteries, more transmission—but also making better use of the demand we already have?

That’s the idea behind demand flexibility. Instead of reducing electricity consumption, we shift it. Industrial loads, EV charging, air conditioning, and other flexible demand can be moved away from peak hours, reducing stress on the grid and allowing more renewable energy to be absorbed.

In other words, maybe the solution to India’s power problem isn’t just generating more electricity. It’s consuming it more intelligently.

We explored this idea in The Daily Brief. Shameless plug, but I linked reading on it.

Govt’s collateral-free export credit scheme finds limited takers (link)

I was reading this Business Standard report on how the government’s collateral-free export credit scheme has found very few takers. And honestly, the headline itself was interesting to me.

At first glance, you’d think this is the kind of scheme people would line up for. If you’re a small exporter, and the government is helping you get a loan without collateral, that sounds like an obvious win. Access to credit is one of those things we keep saying MSMEs struggle with, so a scheme that solves exactly that should, in theory, be popular.

But the numbers suggest otherwise. According to the report, only 140 exporters have registered for the collateral-free export credit scheme since January. Meanwhile, another scheme under the same Export Promotion Mission — an interest subvention scheme — has seen far more traction.

And that contrast is where the nuance lies.

An interest subvention scheme is much easier to understand. You already have a loan, or you’re taking one, and the government absorbs a part of your interest cost. The benefit is direct. Your borrowing becomes cheaper. You can immediately see what you are getting out of it.

A collateral-free guarantee scheme works differently. The government is not giving the exporter money directly. It is giving comfort to the bank. The idea is: if the exporter does not have enough collateral, the government guarantee should make the bank more willing to lend. So the benefit to the exporter is indirect. It only works if the bank actually uses that guarantee to lend more, lend faster, or ask for less collateral.

That is a much harder thing to pull off.

So one tempting conclusion is: maybe exporters don’t really have an access-to-credit problem; maybe their bigger problem is the cost of credit. That would explain why the interest subvention scheme is getting more attention.

But I don’t think we can go that far.

Because we have seen credit guarantee schemes work in other places. ECLGS, for instance, was also a guarantee-backed scheme, and it was far more successful. The difference is that ECLGS was a top-up on existing loans. Banks already knew the borrower. The paperwork was easier. The government guarantee was stronger. And because it came during a crisis, everyone — banks, borrowers, and the government — had an incentive to move fast.

This export credit guarantee scheme is trying to solve a tougher, more structural problem. It is aimed at a narrower universe of MSME exporters who may not already have easy access to collateral-backed credit. It also depends heavily on bank behaviour, awareness, documentation, and last-mile handholding.

So maybe the right way to read this is not that exporters don’t want collateral-free loans. They probably do.

It is that this particular scheme is a slower solution to a harder problem. Interest subvention is low-hanging fruit: make an existing loan cheaper. ECLGS was also relatively low-friction: give an existing borrower a top-up. But getting banks to lend to smaller exporters without collateral is a more complicated intervention.

That’s what made the story interesting to me. The headline makes it sound like exporters are ignoring a good scheme. But the real question may be whether the scheme is solving the right problem in the right way.

SBI joining syndicate for acquisition financing is a big deal (link)

So, SBI is joining the syndicate of global banks which will finance Sun Pharma’s $11.75 billion acquisition of Organon. It looks normal, but it isn’t.

Until very recently, Indian banks weren’t really allowed to finance mergers and acquisitions. It was a strange quirk of regulation. If a company wanted to borrow money to build a brand-new factory, banks could lend. But if the same company wanted to buy another business that already owned factories, employees and customers, banks largely couldn’t finance that purchase.

The reasoning made a lot of sense decades ago. In the 1960s and 70s, policymakers worried about large business houses becoming too powerful. If banks freely financed acquisitions, a handful of industrial groups could simply borrow their way into buying competitors, concentrating economic power even further. Restricting M&A financing was one way of preventing that.

But India’s corporate landscape has changed considerably since then. Competition has deepened, regulation has matured, and many bankers argued that the old restrictions had outlived their purpose.

More importantly, M&A financing is a lucrative business. Since Indian banks couldn’t participate meaningfully, global banks ended up capturing a large share of these deals whenever Indian companies acquired businesses overseas.

When the RBI finally eased these norms, SBI Chairman C.S. Setty was among the most vocal supporters of the move. He openly welcomed the decision, pointing out that Indian banks had long been missing out on an important business opportunity while foreign lenders stepped in.

Which is why this headline stood out to me. SBI joining the financing syndicate isn’t just about how Sun Pharma is paying for its acquisition. It’s one of the first visible signs that Indian banks are finally beginning to participate in a business they had been locked out of for years.

This is a big win for Indian banks :)

What Manie is reading

Equator Mag, The King of Fruits (link)

Equator has been publishing some impressive writing and reporting lately. A few weeks ago, I read a piece by US-based economist Mona Ali from the same magazine on what the Strait of Hormuz crisis means for American power, and I recommend it.

This one is different, though. This one’s a first-person account of a white-collar Chinese worker: his hopes, dreams, where they get realized and where they don’t. And when you read between the lines of what is clearly a micro-account of one individual, you can very much view forces at play that are much larger and more systemic.

This account is about Li Tian, who used to be an IT professional in China. He worked the infamous 9-9-6 schedule that many companies in China are known for: 9 am to 9 pm, 6 days a week. That, as you may know, is primarily a product of how cut-throat competition is in the Chinese economy, where in the complete absence of profits, companies have little choice but to get more work from its employees.

Tian left his job, and the country, and emigrated to Laos. It was partly because his to-be wife lived there, and partly because he smelled a massive economic opportunity: becoming a very specific type of farmer.

China is the biggest importer of a peculiar fruit called durian. It’s often termed “the king of fruits” in South-East Asia, and China makes up 90% of the market for durian. That, in turn, has attracted Chinese investment in durian farms that are primarily located outside China. Tian was swept away by this wave. But durian isn’t easy to farm: it takes years for the first proper harvest, and profits can be high. But until that time, it’s just money burnt, and as Tian says, many Chinese people have come in and given up because they couldn’t deal with the uncertainty of a harvest succeeding or not.

Laos, it seems, has a lot of Chinese people. That is also reflective of the fact that Laos and China have always had strong relations, primarily because they both, at least in name, share a similar ideology. China is Laos’ largest investor and creditor — many of the Belt and Road projects were located in Laos, including a high-speed rail connecting both countries.

Here’s Tian talking about China bringing its cut-throat competition (or neijuan) to Laos:

“It’s we Chinese who have brought the neijuan mentality to Laos. Chinese entrepreneurs dominate in most economic sectors. They control banana, watermelon and durian plantations – the country is still predominantly agricultural – and have also set up many fertiliser factories; they own some of the largest supermarket chains; they sit in hardware stores and grocery stores; they run bars, karaoke clubs and guesthouses.”

Tian outlines what he gets in Laos, and what he doesn’t. Labour there is cheaper, and the climate there is suitable for durian plantation. But Laos has poor irrigation systems, and while the climate works for farming an exotic fruit, it is characterized by oppressive summer heat. It doesn’t have China’s world-class food delivery or ride-hailing or infrastructure.

Perhaps what’s even more telling is Tian’s parents’ reaction to his decision to quit his job in China. When they learnt that he was going to buy a farm in Laos instead, they were pleased. Famously, in China, all land is state-owned. You operate on a lease it gives you, and those lease amounts have become steep.

It’s a fascinating account that also gives you a glimpse of China’s growing influence on the world, and how the internal features of its economy determine what it does outside.

What Bhuvan is building

This Indian Life, Why the rupee fails (link)

Money is front and centre in a lot of our daily decisions. And the two things that feel especially visceral to people are currency movements and inflation.

In the post-pandemic period, we had a resurgence in inflation that eventually subsided. At the same time, the rupee remained more or less stable because of a variety of policy choices.

But over the last year or so, the rupee has depreciated sharply, and this has led to a lot of noise, for lack of a better word.

The rupee depreciating is a problem. It directly hits Indian consumers where it hurts: in the pocket. But at the same time, this recent bout of depreciation has also led to a lot of nonsensical and, frankly, idiotic takes about what exactly it means.

We are a country with very little effective literacy, so expecting widespread economic literacy is perhaps asking a little too much.

So I figured that, with the help of Claude, I would pull together all the relevant data on the rupee and other associated metrics and write a story explaining why the rupee goes up and down, what it means when it rises or falls, and whether a depreciating rupee automatically makes you poorer.

Why does our currency have to depreciate? Who gains and who loses when it does? And what does any of this actually mean for the average Indian?

This is my attempt to demystify currency movements and explain what they really mean.

We have a book club!

Here’s another reminder of something that we’re pretty bad at advertising: our book club.

So here’s an image of our fairly-impressive book collection to attract you. Yes, they’re not just for show, and we do read them, alongside some coffee/tea and sandwiches.

The Markets book club has been running for nearly a year. We have some avowed loyalists who come almost every weekend and nerd about their readings with us. But really, it’s become a great spot for many of us to talk to each other - even forge new friendships - without being distracted by any screen. It’s this in-person community that we’re really proud of building.

So, we’d love for you to join us! We host the book club every Saturday, 10:30-1 pm, in JP Nagar 4th Phase. Unfortunately, this location is fixed - we understand JP Nagar may be far for some. But this is the only place where we can host it smoothly. And we don’t host sessions online, either.

If you’d like to attend the book club, please keep the above in mind, and please reach out to: pranav.manie@zerodha.com!

Can you conduct the book club in an online setup?? I'd love to join the club but I'm based in Kanpur.